Industry Outlook

July 2025

Constructive M&A Outlook for Remediation Services

M&A for 2025 and the foreseeable future is positive and increasingly attractive, particularly for both strategic and private equity buyers. The sector is part of the broader industrials and services landscape, which is seeing renewed M&A interest as macroeconomic conditions stabilize and as companies seek growth through acquisitions.

001

001

The Industrials & Services Landscape in 2025

Why Industrials & Services are in Demand

Strategic M&A is Accelerating. Large corporate and private equity buyers are actively seeking acquisitions to strengthen core capabilities, expand service offerings, and accelerate digital transformation. The focus is on businesses that enable energy transition, automation, and operational efficiency.

Reshoring and Supply Chain Resilience. Ongoing geopolitical uncertainty and lessons from recent disruptions have made supply chain resilience and domestic manufacturing top priorities. Companies with automation, advanced manufacturing, or facility management capabilities are particularly attractive.

Fragmentation Means Opportunity. Many industrials and services subsectors remain fragmented, creating robust roll-up opportunities for buyers looking to build scale and market reach.

What do Buyers Want?

In the broader industrial and service sector three drivers prevail. They include 1) modernization and technology, 2) recurring revenue and diversification, and 3) operational excellence.

First, buyers are prioritizing businesses that have invested in automation, digital tools, and data-driven operations. Demonstrating tech enablement and a clear path to further digital transformation will set your company apart. Secondly, service businesses with retainer-based contracts, long-term supply agreements, and a diversified customer base are commanding premium valuations. Predictable income streams and reduced client concentration are key value drivers as well. Finally, streamlined operations, scalable processes, and a strong management team are essential. Buyers look for businesses that can integrate smoothly and sustain growth post-transaction.

Summing it all up for the broader sector, the second half of 2025 is shaping up to be a time of renewed growth and robust deal activity in industrials and services. With careful preparation and a tailored approach, founders can capitalize on this dynamic market and achieve a successful, value-maximizing exit.

Constructive Outlook for Remediation and Related Services

The Remediation sector is part of the broader industrials and services landscape, which is seeing renewed M&A interest as macroeconomic conditions stabilize and as companies seek growth through acquisitions.

Buyers are targeting cleanup, waste, and technical consulting firms, spurring an M&A boom in remediation and environmental services.

Why? As we move through 2025, the landscape for M&A in remediation services and adjacent environmental sectors is more dynamic—and attractive—than ever. Founders and owners in these industries are seeing heightened interest from both private equity and strategic buyers, driven by a confluence of regulatory, economic, and societal trends. Here’s an in-depth look at what’s fueling this surge, what buyers are seeking, and how related industries—waste management, construction, and technical consulting—fit into the picture.

Why Remediation and Environmental Services are in the M&A Spotlight

For starters, remediation and environmental cleanup services are considered essential and non-discretionary. Whether it’s the aftermath of a natural disaster, the discovery of hazardous waste, or compliance with new environmental regulations, these services are required regardless of broader economic cycles. This resilience insulates the sector from macroeconomic uncertainty and makes it a defensive play for investors.

Moreover, heightened government scrutiny and public awareness around environmental issues—especially concerning “forever chemicals” (PFAS), water quality, and climate change—are driving demand for remediation, waste management, and technical consulting services. The Biden-Harris Administration’s increased regulation on hazardous substances, along with ongoing EPA actions, has created a steady pipeline of projects that require specialized expertise and compliance.

The remediation, waste, and environmental services sectors, additionally, remain highly fragmented, with thousands of small and mid-sized operators across the U.S. This fragmentation creates fertile ground for roll-up strategies, where buyers acquire multiple businesses to build regional or national platforms, achieve economies of scale, and expand service offerings.

Lastly, the construction market’s recovery and expansion—particularly in commercial and industrial segments—are fueling demand for remediation and environmental services. New builds, renovations, and infrastructure projects often require site assessments, hazardous material removal, and ongoing environmental compliance, creating a steady flow of business for remediation and consulting firms.

Who’s Buying?

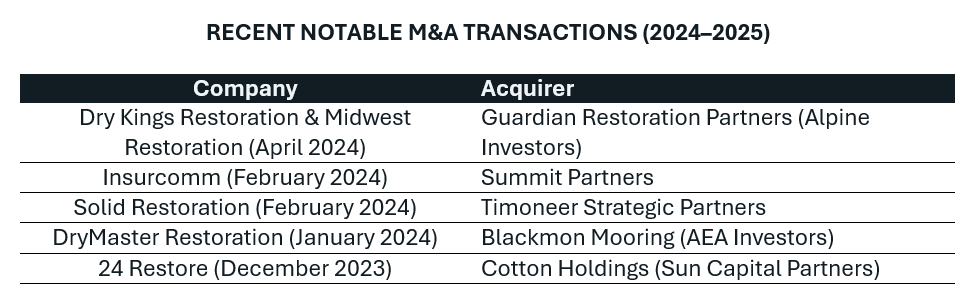

Private equity firms are leading the charge, aggressively forming platforms and executing add-on acquisitions. Recent deals include Kohlberg & Company and Partners Group-backed BluSky Restoration’s acquisition of Mammoth Restoration, and Trivest Partners-backed HighGround Restoration’s purchase of Expert Water Removal. These platforms are seeking to build scale, diversify services, and create exit-ready businesses for future PE or strategic buyers.

Further, large national and regional players—such as GFL Environmental, Republic Services, and Veolia—continue to consolidate the market, acquiring smaller operators to expand their geographic reach and service portfolios. These companies are particularly interested in firms with strong regulatory relationships, specialized technical expertise, and recurring municipal or industrial contracts.

The trend isn’t limited to traditional waste or remediation companies. Construction giants, engineering firms, and even international investors are entering the fray, seeking to add environmental capabilities to their service mix or capitalize on the U.S. market’s regulatory and infrastructure-driven growth.

Adjacent and complementary sectors are in play as well. Waste management—especially in liquid waste, hazardous waste, and recycling—has seen robust M&A activity. The recurring nature of waste contracts, combined with increasing sustainability mandates, is drawing both public and private buyers. Companies are innovating by turning waste streams into biofuels, energy, and other value-added products, further increasing their attractiveness.

This includes construction and site preparation construction firms which are actively acquiring remediation and environmental consulting businesses to offer turnkey solutions for complex projects. The push for sustainable building practices, digital transformation, and integrated project delivery is driving deals that combine construction, environmental, and technical expertise under one roof.

Technical and environmental consulting firms specializing in environmental compliance, permitting, and engineering are in high demand. Buyers value their recurring revenue from long-term contracts, regulatory expertise, and ability to cross-sell services. Notable deals include Oak Hill Capital-backed Trinity Consultants’ acquisition of WestLand Resources, expanding their capabilities in water and ecology markets.

Key Trends Shaping M&A Activity

Consolidation and Platform Building. Buyers are looking to create “full menu” service providers with national footprints, capable of handling everything from emergency response and hazardous waste disposal to long-term environmental monitoring and compliance. This one-stop-shop approach is a major draw for large clients and government contracts.

Technology and Innovation. Digital tools, data analytics, and automation are becoming differentiators. Firms that have invested in technology—such as advanced monitoring, reporting, or remediation techniques—are commanding premium valuations, as buyers seek to future-proof their platforms.

Sustainability and ESG. Environmental, Social, and Governance (ESG) considerations are now central to dealmaking. Investors are prioritizing companies that can demonstrate sustainable practices, regulatory compliance, and a positive impact on climate and communities.

Favorable Capital Environment. With liquidity constraints easing and valuation gaps narrowing, the latter half of 2025 is shaping up to be a year of action. Private equity’s substantial “dry powder” and improved access to financing are fueling competitive processes and strong multiples for quality assets.

Once again, M&A activity in remediation services and related environmental sectors is robust, with potent tailwinds from regulation, sustainability, and infrastructure investment. Whether you operate in cleanup, waste management, construction, or technical consulting, the market is ripe for founders considering an exit. By understanding the trends, preparing your business, and aligning with buyer expectations, you can capitalize on this unprecedented window of opportunity—and achieve a successful, value-maximizing transaction.

M&A Valuations for Remediation Services and Related Services

M&A valuations for remediation services and related environmental services (including waste management, environmental cleanup, and technical consulting) have remained strong in 2024 and early 2025, reflecting robust demand and intense buyer interest. We anticipate momentum to continue throughout the year and the foreseeable future.

If you’re a founder or executive in the remediation services sector or a related environmental, waste, or industrial services business, understanding current M&A market dynamics is essential for strategic planning. The first half of 2025 has seen continued strong buyer interest, deal flow, and evolving valuation trends across remediation, waste management, and environmental services.

The median EV/EBITDA multiple for strategic deals in environmental services (which includes remediation) was 8.1x in the first half of 2024, down from the unusually high 15.1x seen in 2023 as the market normalizes. Private equity buyers have historically paid similar or slightly higher multiples for platform assets, though specific Q1 2025 data for PE deals is limited. Correspondingly, revenue multiples for environmental services and remediation businesses typically range from 1.3x to 1.4x for both strategic and private equity buyers, reflecting the sector’s recurring revenue and regulatory-driven demand.

Fueling this momentum are such value drivers of Recurring, non-discretionary revenue (insurance, municipal, or industrial contracts); regulatory compliance and ESG positioning; automation, technology adoption, and sustainability initiatives; and geographic reach and vertical integration.

Summing it Up

A Seller’s Market for Quality Companies

For owners of remediation, environmental, and waste management businesses, current M&A multiples remain attractive, especially for companies with recurring revenue, regulatory expertise, and a commitment to automation and sustainability. The market is seeing robust deal flow, with both strategic and private equity buyers competing for assets that can drive growth, efficiency, and compliance in an increasingly regulated landscape.

So, if you’re considering an exit or recapitalization, now is an opportune time to benchmark your business against these market multiples and recent deals—and to position your company for maximum value in a competitive M&A environment.

ABOUT ENCORE AMC PARTNERS

Encore AMC Partners is a premier M&A advisory and management consulting firm headquartered in Newport Beach, California, distinguished by decades of hands-on experience as both executive operators and investment bankers. Our team’s unique blend of operational leadership and technical transaction expertise enables us to deliver strategic guidance that is both empathetic to founders’ objectives and rigorously focused on value creation.

We serve small to mid-market companies across a range of industries, providing tailored M&A advisory, exit strategy planning, and management consulting services designed to maximize shareholder value and support lasting legacies.

THE M&A DEAL TEAM ENSEMBLE

Encore AMC Partners is comprised of a core M&A advisory team and a management consulting team.

The firm’s advisory team, below, has a combined 100+ years of multifunctional M&A experience from both sides of the table. The senior partners have led M&A as C-suite operators and as M&A advisors, making us uniquely qualified to create a market because we speak the language of both buyers and sellers.

BUILDING A NO-STRINGS RELATIONSHIP WITH AN M&A ADVISORY FIRM

Establishing a relationship with a trusted M&A advisory firm is a strategic asset for any business, regardless of whether an exit strategy is an immediate priority or a long-term consideration. Whether your goals include a near-term sale to a strategic buyer, a private equity recapitalization, a management buyout, or a future generational transfer, having an experienced advisory partner ensures you are prepared to maximize value, navigate complex negotiations, and capitalize on opportunities as they arise. Proactive engagement with an M&A advisor not only positions your company for successful execution when the time is right, but also provides ongoing market insight, valuation benchmarking, and strategic guidance that can enhance growth and shareholder value at every stage of your business journey.

COST?

Nothing! Building a relationship with us doesn't cost you anything. We only get paid when you are successful when we help you successfully realize your objectives.

Send us a note to learn more!